Purchasing an insurance policy enables us to shift the financial risk of paying for certain losses to an insurance carrier in exchange for the premiums we remit. The terms and conditions of the transaction are detailed in a legal contract, or the insurance policy we receive. Knowing how hard it is for consumers to compare and contrast the terms and conditions between different policies, many insurance carriers market their policies by focusing consumer attention on the one part of the transaction they well understand: the cost. Meanwhile, savvy consumers and the trusted advisors who guide them should ask how it is some insurance carriers that sell policies at a cost far lower than other carriers can still earn a profit. Have some carriers developed a secret strategy?

Purchasing an insurance policy enables us to shift the financial risk of paying for certain losses to an insurance carrier in exchange for the premiums we remit. The terms and conditions of the transaction are detailed in a legal contract, or the insurance policy we receive. Knowing how hard it is for consumers to compare and contrast the terms and conditions between different policies, many insurance carriers market their policies by focusing consumer attention on the one part of the transaction they well understand: the cost. Meanwhile, savvy consumers and the trusted advisors who guide them should ask how it is some insurance carriers that sell policies at a cost far lower than other carriers can still earn a profit. Have some carriers developed a secret strategy?

Their Secrets Revealed

One strategy some carriers use to lower the cost of coverage while maximizing their profits is to issue policies that protect consumers from fewer risks. This works quite well, as the subtle yet important differences in the policy language (the proverbial “contract fine-print”) that detail the risks that are and are not covered by different insurance policies is very hard for consumers to discern. Another strategy some of these carriers use to maximize profits is to adopt claims practices that make it extra difficult for claimants to be reimbursed for losses that are covered. In this scenario, aggrieved policyholders seeking payments that have been denied for losses that are covered by their policies must rely upon state regulators and the legal system to determine if the claims practices used by such carriers are or are not consistent with the terms of the contract. For the many policyholders who do not experience a loss, both of these strategies can be dismissed as “no harm, no foul”. Until a loss occurs.

A Simple Formula To Make Better Decisions

Consumers wishing to avoid learning these lessons the hard way — after a loss for which coverage is either deficient or inexplicably denied —- can be assured the remedy is both simple and logical: conduct better research! Here’s the simple two step formula:

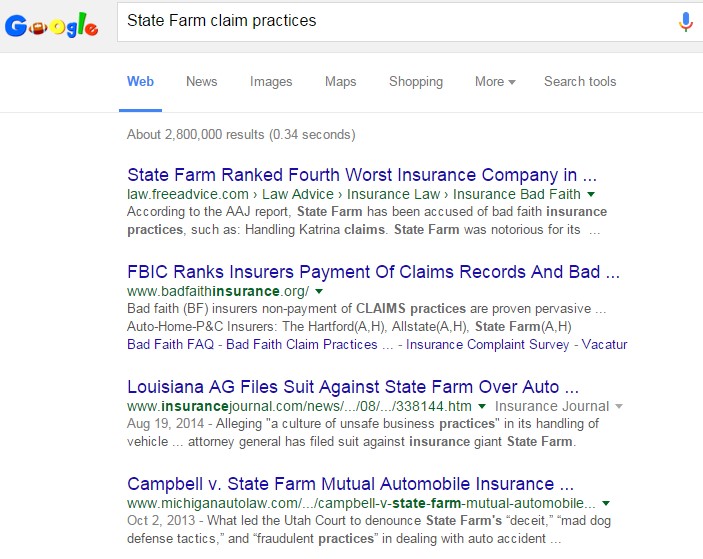

- Enter the name of your insurance carrier (or a carrier are considering) in your search browser and then add these two words: “carrier’s name claim practices”.

- Carefully examine the content on some of the sites revealed by the search to better understand that carrier’s approach to responding to the claims of their policyholders.

That’s it – just taking those 2 steps can arm consumers with important insights needed to make better-informed decisions and begin selecting coverage from insurance carriers that is actually worth paying for!

Why use the words “claims practices” in your search? Again, more important than knowing the cost of coverage is to learn if the insurance you are paying actually honors their contractual obligations! Do not rely on popular who-is-the-best-carrier survey results, as those findings include a number of less important criteria that are not reflective of a carrier’s claims paying practices. Instead, research the two words that will reveal important insights on an insurance carrier’s claim practices and examine the far more revealing insights.

Search Results Can Be Eye-Opening!

The time-honored business practice of “not speaking poorly of competitors” is one I understand and respect. To remove the appearance of bias and finger pointing, I encourage consumers to use the power of the internet to perform the above search for ANY insurance carrier. To illustrate the revealing insights that can be gained, consider just the first few results that appear in the screenshots below for a search on the two companies that insure more homes and cars than any other carriers in the United States.

To be fair: these carriers are often able to save many policyholders hundreds of dollars each year in premiums, just as their advertisements promise. Examining their claim practices can help to explain how they can do so while still earning a profit.

In Conclusion: This information is provided in an effort to arm consumers with the insights needed to make better informed decisions about their insurance protection. To protect ourselves from the shell-game advertising tactics that cleverly shift our focus away from what really matters (being paid after a covered loss) to something of lesser consequence but providing an immediate result we all want (a lower premium), it is critical to conduct better research. On any carrier. Then, read the reviews. Those reviews can often expose the business strategies used by some carriers to fund the “savings” they have advertised to lure your business.

Think I’m making this up? To read an astonishing investigative report that details how State Farm and Allstate contracted with consulting firm McKinsey and Company to reduce their claims costs, simply enter the four words “McKinsey State Farm Allstate” into any search engine. Of all that has been reported about this sordid tale, The Insurance Hoax as reported in Bloomberg News is the most revealing. If you prefer video, check this CNN report by Anderson Cooper available on You Tube.

Let the buyer BeAware!